Content sponsored by:

ABTL Advanced Bio-Agro Tech Ltd

Economic Recession - Recovery and Global Meat Market Dynamics

Published: January 6, 2022

By: ABTL Enzymes

Introduction

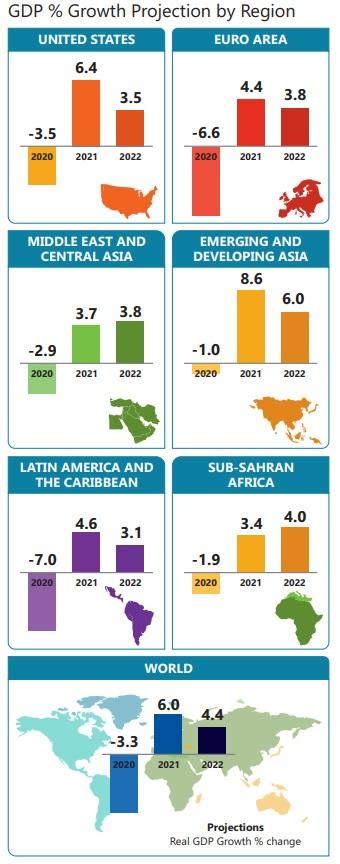

The world economy is experiencing an exceptionally strong but highly uneven recovery. Global growth is set to reach 5.6 % in 2021- its strongest post-recession pace in 80 yearsin part underpinned by steady but highly unequal vaccine access. Growth is concentrated in a few major economies, with most emerging market and developing economies (EMDEs) lagging: while about 90% of advanced economies are expected to regain their pre-pandemic per capita income levels by 2022, only about one-third of EMDEs are expected to do so. In low-income countries, the effects of the pandemic are reversing earlier gains in poverty reduction and compounding food insecurity and other long-standing challenges. The global outlook remains highly uncertain, with major risks around the path of the pandemic and the possibility of financial stress amid large debt loads.

By 2022, global output will remain about 2% below prepandemic projections.

By 2022, output in all regions is expected to remain below pre-pandemic projections, weighed down by the ongoing pandemic and its legacies, which include higher debt loads and damage to many of the drivers of potential output.

The recovery is expected to be strongest in East Asia and the Pacific, primarily due to strength in China. In South Asia, India's recovery is being hampered by the largest outbreak of any country since the beginning of the pandemic. In the Middle East, North Africa, Latin America and the Caribbean, the pace of growth in 2021 is expected to be less than the magnitude of the contraction in 2020, while the tepid recovery in Sub-Saharan Africa will make little progress.

In most regions, risks to the outlook are tilted to the downside. All regions remain vulnerable to renewed outbreaks of COVID-19, which could feature variant strains of the virus; financial stress amplified by elevated debt levels; deeper-than-expected scarring from the pandemic; and rising social unrest, potentially triggered by rising food prices.

With 1.2 billion people and the world's third-largest economy in purchasing power parity terms, India's recent growth has been a significant achievement. Since independence in 1947, a landmark agricultural revolution has transformed the nation from chronic dependence on grain imports into an agricultural powerhouse that is now a net exporter of food.

Since the 2000s, India has made remarkable progress in reducing absolute poverty. Between 2011 and 2015, more than 90 million people were lifted out of extreme poverty.

The International Monetary Fund (IMF) cut India's GDP forecast to 9.5% for the Financial Year (FY) 2022. This is considerably lower than the IMF's previous 12.5% growth estimate for India.

Growth prospects for India for FY22, however, remain higher than all other major economies. As per the IMF, India's GDP is expected to do better than China and the United States.

To build back better, it will be essential for India to stay focused on reducing inequality, even as it implements growth-oriented reforms to get the economy back on track. The World Bank is partnering with the government in this effort by helping strengthen policies, institutions, and investments to create a better future for the country and the people through green, resilient an inclusive development.

China is forecast to grow 8% in 2021 and 5.6% in 2022. It said that China's prospects for 2021 are marked down slightly due to stronger than anticipated scaling back of public investment. And in the long term, demographic challenges in China and other emerging markets make it more pressing to reverse a persistent decline in longterm growth and build a more buoyant post-pandemic global economy.

The recovery is not assured until the pandemic is beaten back globally. Concerted, well-directed policy actions at the multilateral and national levels can make the difference in diminishing divergences & strengthening global prospects.

Economic Recession and Recovery of the two Powerhouses of Asian economy:-

What is the future of meat? Well, it should continue to be produced and consumed, just like it has been. Let's start from the start. Global population is expected to grow to 10 billion by 2050. 2.1 billion more mouths to feed from today. To meet the projected food, demand the answer can hardly be keeping twice as many poultry, 80% more ruminants, 50% more cattle and 40% more pigs, utilizing the same level of natural resources as we currently do. Also, just producing enough food will not be enough. Feeding the world population adequately would also mean producing safe food that ensures nutrition security.

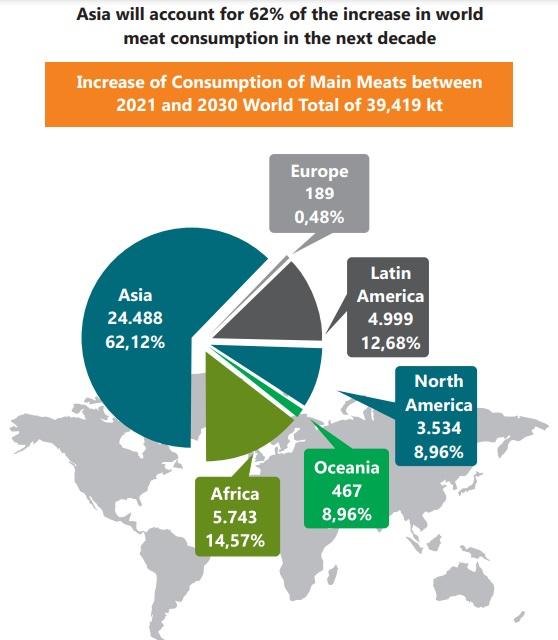

While demand for livestock derived foods is expected to plateau in high income countries, it will grow rapidly in Africa & Asia mostly due to rising populations and rising incomes. As income rise, people will increasingly consume more resourceintensive, animal-based foods.

India will have 1.7 billion people by 2050, creating the most populated country in the world and with the most demand for food – an increase of a staggering 70%. Consumer spending will increase significantly, as more Indians move up the economic ladder. If you are in India, you are seeing the meat consumption is on the rise, and not in a small way.

Meat consumption has been shifting towards poultry. In lower income developing countries this reflects the lower price of poultry as compared to other meats, while in high-income countries this indicates an increased preference for white meats which are more convenient to prepare and perceived as a healthier food choice. Globally, poultry meat is expected to represent 47% of all the protein from meat sources in 2030, an increase of 2% points when compared to the base period. The global shares of other meat products are lower: beef (11%), pigmeat (36%), and sheep meat (6%).

More than three-quarters of global agricultural land is used for livestock production today, which supplies one-fifth of the world's calories. Additionally, the domestication of livestock has altered the makeup of our ecological systems. Livestock production contributes to 14.5% GHG emissions globally. Livestock will continue to be raised in widely different ways around the world. By accounting for this diversity -in live-stock systems and businesses and their various development trajectories-the rising demand for meat, milk and eggs must be met sustainably.

Meat is big business and supports billions of livelihoods. Many view the aggressive push for alternative protein as an anti-meat agenda. Conventional protein production is fundamental to today's food system. A reduction in animal protein demand would reduce demand for feed crops like corn and soybean, altering the economics of production, putting producers under increasing pressure to diversify production.

Finally, this consumer preferences will evolve according to historical patterns. As a result, dietary preferences for lower meat consumption or for alternative protein sources are assumed to expand slowly and to be adopted by a small part of population concentrated mainly in high income countries, and therefore hardly affect meat consumption over the next decade. Nevertheless, while the competition from substitutes will increase, consumer choice will continue to be influenced by the nutritional content in meat as compared to protein substitutes.

Related topics:

Authors:

Recommend

Comment

Share

Would you like to discuss another topic? Create a new post to engage with experts in the community.

Featured users